Greenlight vs GoHenry vs FamZoo – Choose BEST Kids Debit Card for your Kids 2025

Choosing the right kids’ debit card can feel like standing in front of a huge candy store—so many options, so many features, and you want “just the right one.” If you’re looking for the best choice between Greenlight, goHenry, and FamZoo, you’re in the right place. This article dives deep into what each service offers, compares them across features, cost, flexibility, and educational value, and helps you decide which is the best fit for your family. By the end, you’ll know: what your priorities should be, what trade-offs you’ll accept, and which card does what you need.

Disclaimer: The information in this article is for general guidance only. The services mentioned are typically based in the U.S., pricing and features may change, and local availability (including in India or for overseas users) might vary. Always check the latest terms and conditions and consider your own family’s financial circumstances before signing up.

Read More: 8 Effortless ways to get a loan with low credit scores/CIBIL score.

What you want to look for in a kids’ debit card

Before comparing the three, let’s talk about what makes one card better than another. Because what’s “best” depends on what you need.

Parental controls and oversight

You’ll want to control when money is added, where the card can be used, what it can purchase, and get alerts when it’s used. This helps protect your child’s money, but also lets you turn their spending into a learning moment.

Learning & habits

If your goal is more than just “give my kid a card,” you’ll want tools that help your child understand allowance, chores, saving, investing—basically, real-life money habits.

Fees, age & scalability

Monthly cost, number of kids allowed, minimum age, and ability to add multiple cards—these matter, especially if you have more than one child.

Flexibility & features

Does the card just let them spend? Or can they save, invest, set goals, maybe even borrow (under supervision)? Does it support ATM access? International use? Are there extra perks like cashback?

Safety and reliability

You want a card backed by real banking partners, FDIC or equivalent deposit protection, strong security, and a platform you trust.

Detailed Comparison of Each Option

Here’s a quick snapshot of the three contenders.

1. Greenlight

The Greenlight Card is a fantastic way to expose children to the real world of personal money and budgeting. It is an app and a debit card. Children learn things like the difference between wants and necessities in a better way when given their own card to use for savings or purchases.

Users can load money onto the card through the Greenlight app, making it simple for them to check family members’ spending and teach them how to manage their budget.

Although there are other children’s debit cards on the market with reduced fees, the Greenlight card offers incredible value, especially if you have numerous children.

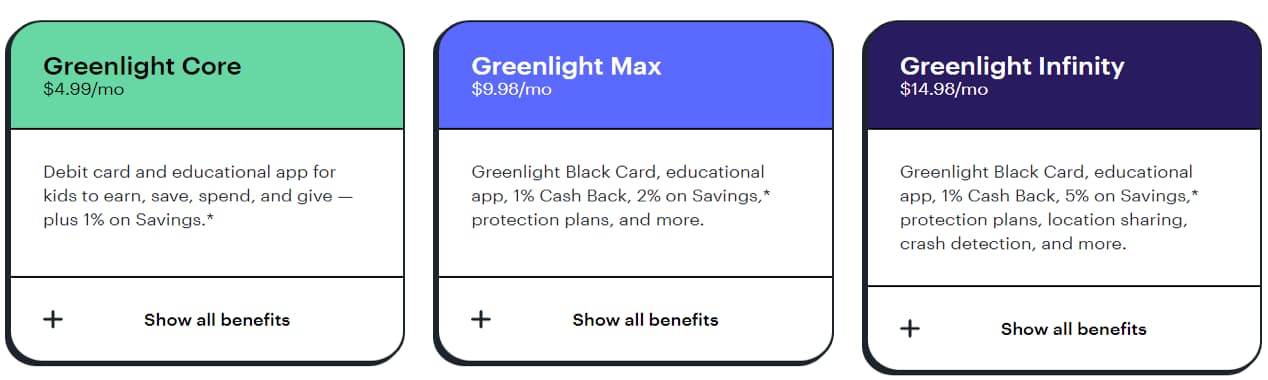

By giving you the feature of setting spending limits on specific retailers, the Green Light Card gives you good control over your child’s spending. It also has cashback incentives, a 1% to 5% annual savings bonus, and a feature that teaches your child the value of stocks, depending on the plan you apply for. Being one of the few children’s debit cards with purchase, identity theft, and mobile protections.

However, these extraordinary services come with a monthly fee. The details of the different monthly plans it offers are shown in the figure.

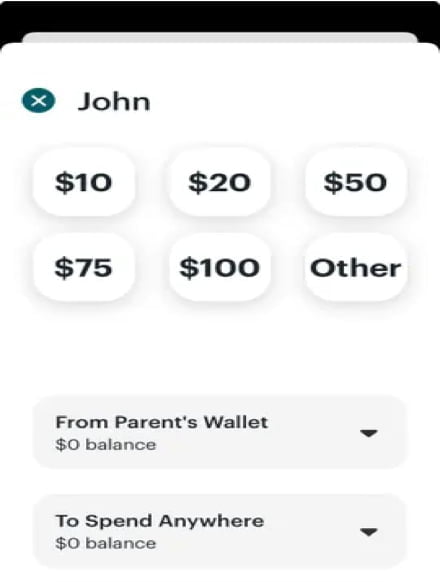

Through their associated bank account or debit card, parents can add money to their Parent Wallet, which is held within the Greenlight App. You will not be able to receive Greenlight Savings Rewards if you choose to link a debit card rather than a bank account.

Click the “Add $” button on the Parents’ Panel to add money from your parent account to your child’s debit card. Teens can set up a direct deposit so that their paychecks are automatically transferred to the card. Look at the figure for the app interface.

Youngsters are entitled to make any transactions they want with their debit card and can use it at any Mastercard-accepting outlet. They can also use ATMs without having to pay Greenlight, but the bank that operates the ATM will impose a fee. Parents can limit how much their youngsters can spend on certain products, such as a $30 restriction on console games, as well as how much they are allowed to withdraw from ATMs. They can do this through the app’s Spend Control section.

When bringing your child on an international trip, you can provide them with some spending money because there are no foreign transaction costs. Furthermore, there aren’t any overdraft fees or minimum balance requirements. This was all you needed to know about the Greenlight debit card, but it isn’t the only debit card available for youngsters. Let’s take a look at its alternatives now.

2. GoHenry

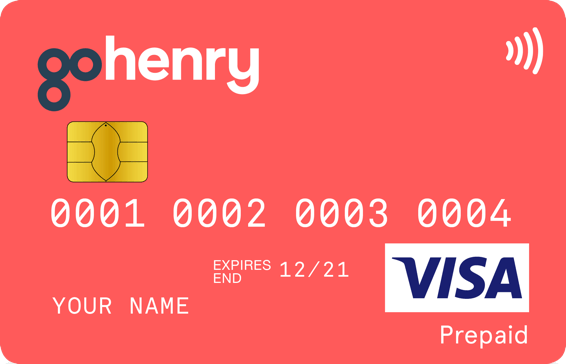

GoHenry is a system designed for youngsters to teach them to learn about money. It is an App that provides them with a debit card, which can be used to make transactions just like any other debit card. GoHenry provides benefits for parents as well, like the ability to quickly manage pocket money, modify parental settings, and much more. Therefore, it’s one of the simplest ways to provide young people with financial knowledge. The figure shows what a personal Gohenry card looks like.

Parents can set savings goals and check their child’s account balance easily by using the GoHenry app. The card can be used online, at an ATM, and directly at retailers. The interesting thing is that all these functions of the card can be controlled by parents from the App.

The system will notify the parents whenever their child uses an ATM or makes any type of purchase. In an unfortunate case, the card is misplaced by the child, the parents, or the child can easily block the card using the App.

GoHenry has introduced a special feature called money missions. Children are offered points and badges for watching informational videos and quizzes that help them learn how to manage their money better.

This teaches the kid about money in a way that they will never forget. They also learn to make good money-saving habits while observing how different pay rates are available for different jobs.

These money lessons will teach the young ones a lot, and they will be able to make better financial decisions when they become adults.

GoHenry is convenient when it comes to pocket money for youngsters. It allows the parents to set weekly allowances and specify where their child should not make any purchases. Thus, it relieves the parents as Gohenry takes on their trouble of overseeing how children spend their pocket money.

It also provides the feature of no debt, which means the child cannot make purchases using bank overdrafts, so the parents don’t have to worry about their young ones overspending and getting into debt.

GoHenry also provides service for international transactions, so even if your child is abroad, you can instantly transfer money to them without any complications. It allows children to develop a sense of financial education and the ability to make their own choices.

3. FamZoo

FamZoo is an online bank system that provides prepaid cards to children and also gives importance to providing financial education to youngsters. FamZoo has many other features that make it more than just a prepaid debit card. This is extremely useful for busy parents.

A special thing about FamZoo is the customer service it provides. Customers are connected with an expert who has good knowledge about the service. Being denied proper customer service due to short staffing is impossible when you are a customer of FamZoo.

Famzoo was the first to introduce novel features like parent-paid compound interest, tracking for college loans, requests seeking repayment, family invoicing, and many others. It also has a user-friendly interface, so everyone is able to easily use it. Famzoo has introduced the FinLit card. This will teach your child how to manage their money by building solid habits into them.

Famzoo never compromises on the quality of service it provides. They are privately owned, self-sufficient, and individually financed. This means that neither the equity market nor investment firms will push us to put growth above service and education.

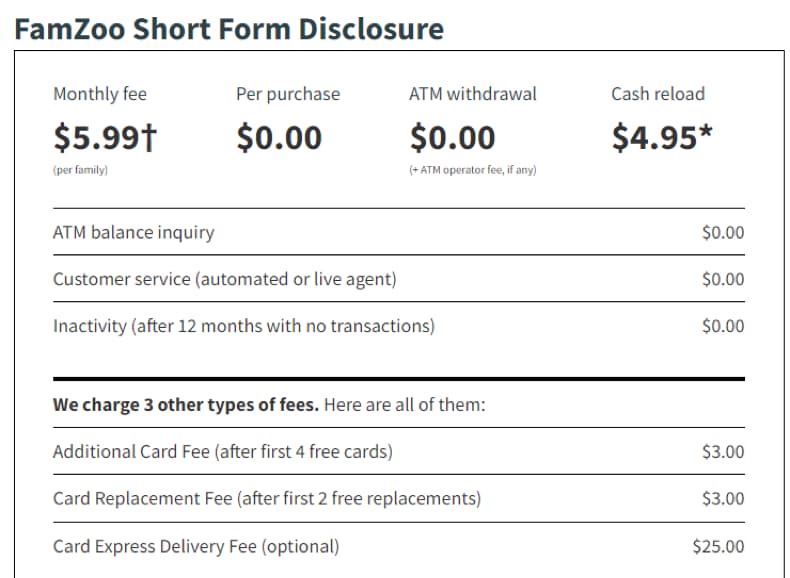

Famzoo provides multiple plans, each with a different level of service. It has a subscription fee per family. The number of family members or cards is unrestricted. Therefore, the deal is better for the larger family. Additionally, highly discounted pay-in-advance programs are beneficial to families of all sizes. Here is an example of a plan it is offering.

Each of these systems provides great services to its customers and has created a big audience by doing so. Thus, it can’t be just said which card is best among them, as everyone has their preferences. If anyone is having difficulty choosing, they should consider reading this article again and see whose services and charges are feasible for them.

FAQ

Q1: My child is only 5 years old. Do these cards still make sense?

Yes, they can. For a 5-year‐old, you’ll mostly use the card as a tool to teach “money exists” and “you decide whether to save or spend”. Choose a card that allows very parental control and is simple. goHenry or FamZoo may work well; you might slowly introduce Greenlight’s advanced features later.

Q2: What happens if the child tries to spend more than available funds?

All these platforms are prepaid/debit style: the card will decline if there’s no money. That’s part of the lesson — unlike a credit card, you can’t overspend. Make sure your funding schedule is consistent so they have money only when you budget it.

Q3: Is investing through a kid’s card safe or encouraged?

It can be safe if done with guidance. Greenlight offers investing (with parental approval). But remember: investing involves risk, and for kids, the goal is learning more than maximizing returns. Always supervise and ensure the child understands the concept of risk, long‐term vs short‐term.

Q4: Can I track the child’s spending even if they are at school or abroad?

Yes—most of these apps offer real‐time transaction alerts or notifications on your phone whenever the card is used. That way, you’re always “in the loop”.

Q5: How much should the allowance be?

There’s no one size. It depends on your budget, your child’s age, what tasks they do, and your family values. Use the card to tie allowance to chores or goals. For example: “If you do X chores, you’ll get Y amount loaded this week.” The card becomes the vehicle, not the goal.

Q6: Can the card work internationally (for travel) and withdraw cash?

It depends on the card and plan. Greenlight, for example, works with many ATMs, but ATM owner fees may apply. If you plan to travel or your child will use it abroad, check foreign‐transaction fees, currency conversion, and ATM access. For users in India, also check whether the motherboard banking partner allows such usage.

Q7: My child already has a bank account; is a kids’ debit card still useful?

Yes—especially if your goal is teaching money management early and you want strong parental controls. A kids’ card app is often more tailored to learning, allowing chore/allowance automation, savings goals, spending categories, etc. If your existing account lacks these, a kids’ dedicated platform adds value.

Conclusion

If I were speaking as a friend,d: if you want all the bells and whistles and will use them (investing, rewards, fine-grained controls) and you have multiple children, go with Greenlight.

If you have one child (ages 6-10) and you want something simple and effective with a moderate cost, goHenry is very solid.

If your focus is practical life lessons—saving, spending, allowance, loaning between siblings—and you want cost-effective with fewer extras, FamZoo is a very good pick.

Given your location (in India) and if you are looking for global or India-friendly usage, you’ll want to check whether each service supports your country or funding method. Once you confirm that, pick the platform whose feature set aligns most with your family’s goals.

Teaching kids about money early is one of the greatest gifts you can give them—and using one of these card platforms can make it tangible and real. Choose the tool that lets you lead the lesson, and let your child discover the fun of managing their own money with your guidance.